Benefits Platform

The digital one-stop-shop for managing your benefits

Swibeco centralises all your employee benefits easily and efficiently. Including administration and automatic rewards, all completely tax free.

Financial well being

Engage your staff with a tangible increase in purchasing power

Permanent discounts that make a difference! Whether it’s food, fashion, insurance, multimedia, cars, travel or gas, we have what your employees want. And our points system, 100% exempt from social security contributions and taxes, will also increase their financial well-being.

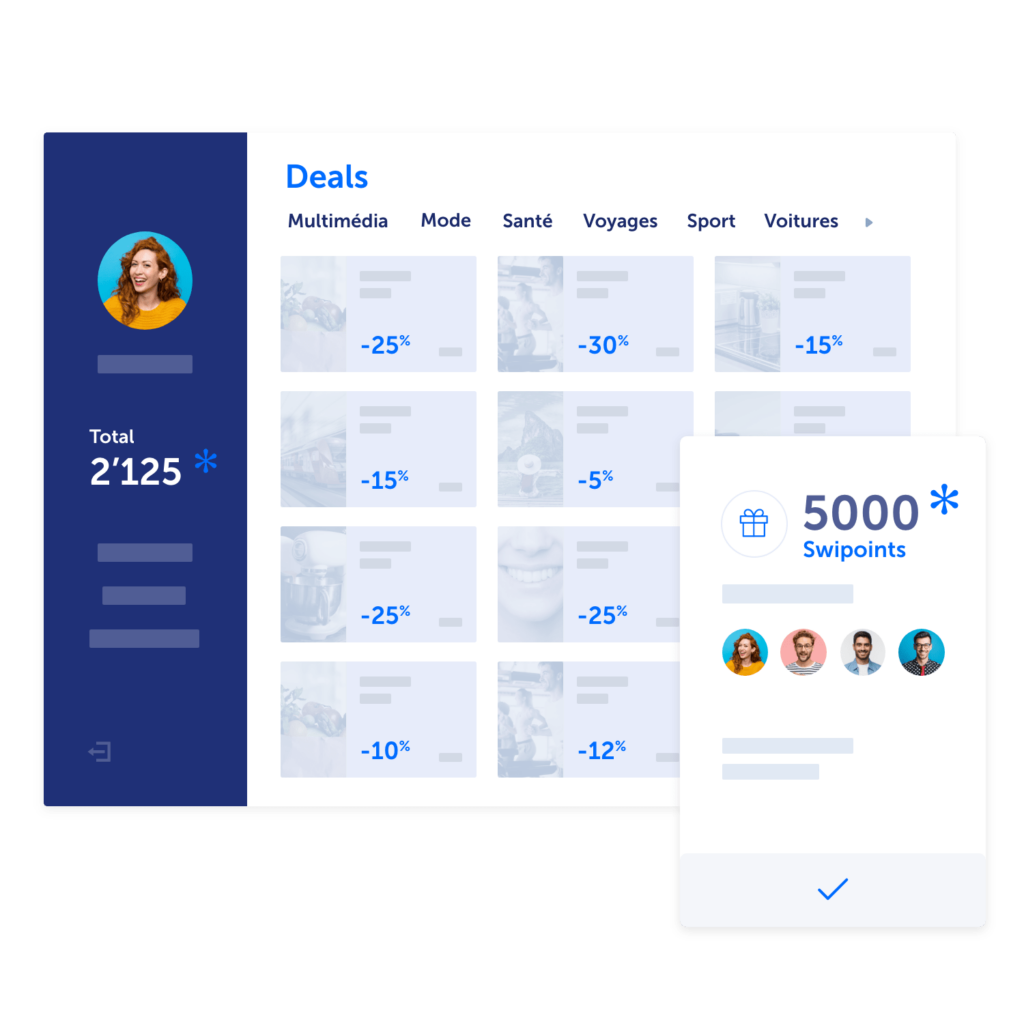

Full flexibility

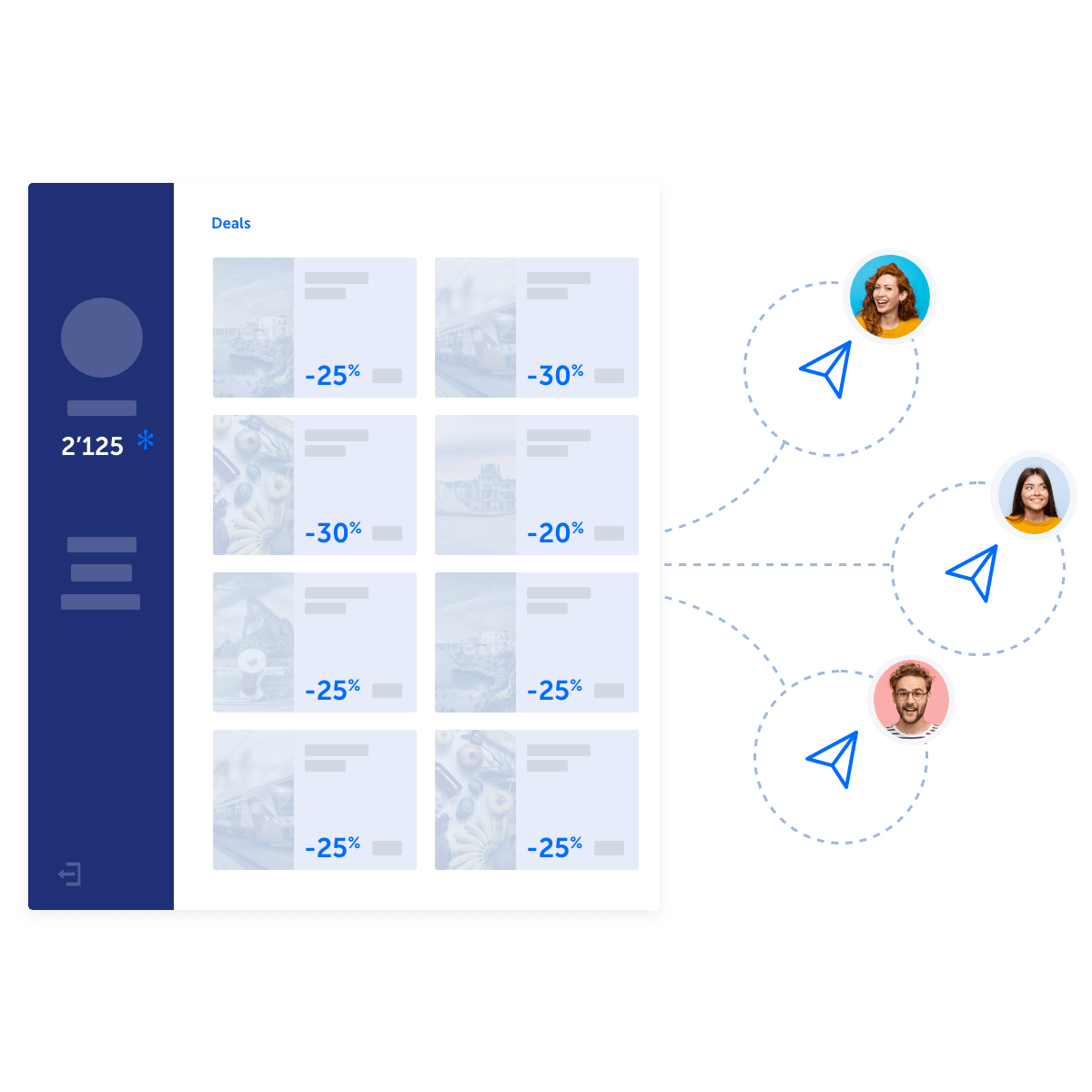

You provide benefits, your employees choose how to use them

Reward your employees with Swipoints. They can use their credit on the Swibeco platform at any time, for instance to purchase discounted vouchers from a variety of brands. Letting employees use their points according to their needs and desires is what Swibeco’s “flexible benefits” is all about.

Outsourcing

Outsource negotiation, integration and monitoring of new partners

When you choose Swibeco, your benefits options are constantly updated. We take care of negotiating, integrating and monitoring new offers, as well as getting the word out. You can also transfer free of charge all of your current benefits to your Swibeco platform.

![]()

White label

You can easily customise the Swibeco portal with your corporate colours, images and logo, providing a familiar experience for your employees. All in just a few clicks!

![]()

No installation required

Everything happens on the Cloud, making it fully compatible with your current systems. No installation or new technology! You even get a unique, personalised URL.

![]()

Secure

With highly secure servers based in Switzerland, we guarantee worry-free data processing. We own 100% of our technology and do not transfer any of your data.

![]()

Integration with HR systems

To make administration of the platform more efficient, our Swibeco solution can be easily integrated with any existing HR Information System (HRIS).

![]()

Compatible with all devices

Keep your benefits at your fingertips with a platform accessible at all times on our website as well as our iOS & Android apps.

![]()

Customer support

We help you roll out your new benefits programme and tell your employees about it. Our dedicated team provides support as you develop your employer brand.

![]()

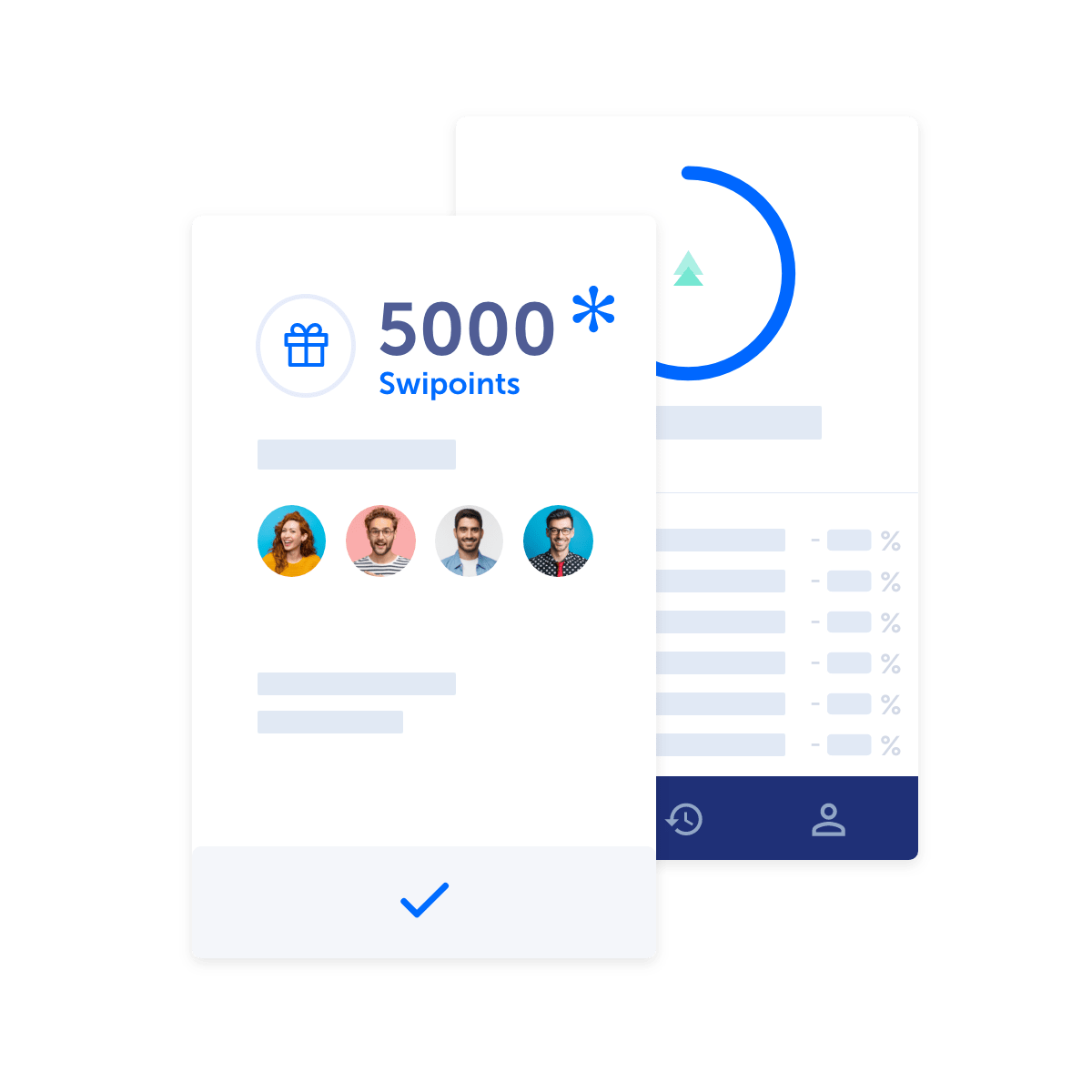

Points system

Swipoints

Give out Swipoints as rewards or gifts. Your employees can then use these 100% tax-free points to pay for a wide range of benefits. How they use their credit is up to them. They can buy products or discounted vouchers from a variety of brands.

Fully tax free

Swipoints are considered gifts under articles 2156, 2157 and 2158 in the “Directive on the determining salary in the AHV, IV and EO” of the Federal Social Insurance Office and article 3 in the “Guide to the preparation of the salary certificate and the pension certificate” of the Federal Tax Administration. As long as you give out Swipoints for recurring and non-recurring events, you don’t need to declare them on the salary statement. By law, you are allowed to accumulate several gifts per year and per employee. More details in the applicable legal framework below.

Governing legal framework

Flexible Benefits

La valeur ajoutée du système de points réside dans leur utilisation flexible et individuelle. Chaque collaborateur décide ce qu’il veut s’offrir avec les montants reçus, selon ses besoins et envies. C’est le principe des “flexible benefits“ de Swibeco!

![]()

Types of offer

Everyone loves discounts and saving money

We have something for everyone: multimedia, fashion, telephony services, sports, food, gas, travel and much more. Swibeco offers deals from over 150 top cooperation partners, always at the best conditions.

Permanent deals

Discounts offered by our partners range from 4% to 35%, using promo codes or gift cards, valid all year round.

Flash deals

With short-term discounts of up to 75%, your employees enjoy even better savings on a regular basis.

In-house deals

If you have already negotiated benefits with local partners, you can add them to your platform; they will only be accessible to your staff.

Love deals

Your employees benefit from permanent discounts at the most popular shops in Switzerland: Coop, Migros, Manor, Zalando, IKEA, Interdiscount, H&M and many more.

Some partner brands that offer permanent discounts

Calculate your savings potential

How much could you save with Swipoints?

Use our simulator to calculate how much you and your employees could save by giving Swipoints as gifts for special occasions such as birthdays, anniversaries, Christmas, etc.

How large is your organisation?

Indicate your total number of employees and find out how much you could save in just a few clicks.

How much do you want to give your employees each year?

With Swipoints, you can reward your employees with up to CHF 500.- each per event (you can schedule multiple events per year). This amount is 100% exempt from social security contributions and taxes.

Are considered as events occasions such as: birthdays, work anniversaries, jubilees, welcome gifts, Christmas.

CHF /year per employee

CHF XXX

Employer

-CHF XXX

Employee

+CHF XXX

*These calculations are based on the following values: employee’s social security contributions 15%, employer’s social security contributions 20% and marginal tax rate (federal, cantonal, municipal) 30%. Non-contractual calculations

Customise your estimate with your company’s data

Social security contributions

Enter your employer and employee social security contributions

Average employer contributions (1st and 2nd pillar)

Average employee contributions (1st and 2nd pillar)

Tax rate

Enter your employees’ average marginal tax rate

View tax rates of your canton.

Click here

Marginal tax rate (federal, cantonal, municipal)

Average annual salary

Enter the average gross annual salary of your employees.

Invalid value

Without additional costs for companies with AXA OPA or DSB contract

Bonus for AXA customers

The use of the Swibeco benefits platform is inclusive for customers with occupational benefits (OPA) or daily sickness benefits insurance (DSB) from AXA. Companies with no OPA or DSB contract get 25% off*.

* Discounts do not apply to the Swibeco Lunch Card

Easy access via myAXA

You can access the platform easily and integrate company and personal data quickly using your myAXA Admin login (www.myaxa.ch). Simply register your company, select your employees, customise your portal and off you go!

3 easy steps

Find out how Swibeco can help you manage your HR benefits and effectively engage your employees. With nothing to install on your end!

Invite employees

Enjoy the benefits

Offering gifts

Start inviting your employees to use their many benefits

Through the Swibeco platform, you can trigger an email invitation to all of your employees so that they can take advantage of the wide range of benefits that you offer them.

Sustainable savings begin

With Swibeco’s exclusive deals negotiated with many major retailers, your employees get preferential treatment, increasing their purchasing power all year round.

It’s so easy to make them happy

When you reward your employees with Swipoints — our points system that is entirely exempt from social security contributions and taxes — you not only give them additional purchasing power, but also the ability to choose how to use their points.

Start your digital HR transformation

Find out how Swibeco can help you manage your HR benefits and effectively engage your employees. With nothing to install on your end!